Service hotline

+86 0755-83044319

release time:2022-03-08Author source:SlkorBrowse:12500

"How many years will it take for China's semiconductors to catch up with the world's level? The answer I gave two years ago was that packaging has basically caught up with the world's level. It will take 5-10 years for design, and 10-15 years for memory. Equipment/materials take 10-20 years, and those with a high threshold will be relatively slow.”

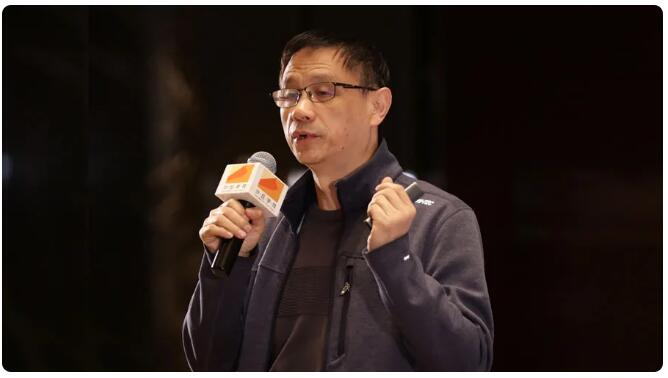

Picture: Chen Datong, Partner of Puhua Capital

Not long ago, mentor Chen Datong came to Dune College to share his insights into semiconductor entrepreneurship and investment in the past 30 years. This article is for desensitization content sharing:

Can investing in China's semiconductor industry make money?

In 2009, I attended the annual meeting of Zero2IPO. At the annual meeting, someone said that investing in all industries in China can make money, except for semiconductors. I have worked in semiconductors all my life, and the stimulation I received at that time can be imagined. I thought to myself, as a rapidly developing industry, is there really no investment opportunity in semiconductors? So, I spent ten years to verify this.

At the end of 2009, we established Huashan Capital. Huashan Capital mainly invests in foreign technology companies. It has also invested in 6 companies in China. Now, 5 of them have been listed, and another one is doing red chips and can also be listed. Zhaoyi Innovation is the first project we invested in in China. When it was listed, it made about 30 times of profit, and now it has about 100 times of return. In 2014, when the country really wanted to make semiconductors, we established Qingxin Huachuang (now Puhua Capital), invested in 16 domestic projects, and also contributed to two very famous international mergers and acquisitions in the semiconductor industry. Now some projects are gradually withdrawing, and the annual return IRR is about 50%. In 2018, we established Yuanhe Puhua together with Big Fund and Suzhou Yuanhe Group. Now we have invested in more than 70 projects, and the paper IRR exceeds 60%. We have proved through practice that semiconductors, as a fast-growing industry in China and an indispensable industry supporting the development of national industries, have many investment opportunities and can make money.

After two successful startups, we turned to investment

I was one of the first batch of college students after the Cultural Revolution. I used to join the ranks in the countryside. After the resumption of the college entrance examination in 1978, I took the exam in Tsinghua University. At that time, I was majoring in radio image information processing in the Department of Electronic Engineering. Later, because of my interest, I transferred to the Department of Semiconductor Physics in the Department of Radio. After that, I was a bachelor, master, and doctorate student. After graduating from my Ph.D., I went to study in the United States. After turning around, I stayed in Silicon Valley, because Silicon Valley is the most concentrated place for semiconductors.

American Entrepreneurship: Founders Who Hit and Hit

In 1993, I joined a US semiconductor company as a senior engineer. For me, the development path to become an engineer is very clear. However, in 1995, a chance came. At the time, a friend of mine wanted to start a company to develop image sensors using CMOS technology and invited me to be a co-founder. In this way, I "passively" started the first business in my life. In the United States, there are only two types of entrepreneurship, one is technology entrepreneurship, and the other is business model entrepreneurship. You have to create new technologies or business models that are not available in the world. If you do something that is too me, you have no chance. We just came across an opportunity for a tech startup. The camera chips of the year were made with a special semiconductor process. This process is called CCD. It was invented in the United States in the late 1960s and was later learned by Japan in the 1970s. After that, Japan completely defeated the United States, because the technology was monopolized by them. In the 1990s, with the development of semiconductor technology, people suddenly wondered whether mainstream CMOS technology could be used to do these things. Later, a lot of experiments were carried out. Around 1995, everyone felt that the technology had developed to a certain extent, and it should be possible to commercialize it. . So in 1995, a lot of startups appeared. The company we founded is called OmniVision, which was also established in 1995. We were a team of a dozen people at the time, and our competitors were a team of hundreds of people such as Intel, HP, and Sony. The first investment we got was about $2 million, and we had to compete with hundreds of millions of dollars. But in the end we won. The development of our technology

Makes the camera function can be installed on today's mobile phones.

In 2000, OmniVision was listed on Nasdaq.

Entrepreneurship in China: A Homecoming Journey

Why go back home? The success of OmniVision has given me great confidence. After the company goes public, I especially want to go back to China. At that time, many people did not understand this. They said that the conditions in Silicon Valley were so good. You can expand your company or start a new business in Silicon Valley. Why do you want to come back? I have given several reasons for this. The first is the global industrial transfer trend, from Europe/US/Japan to [敏感词]/South Korea, and then to the mainland. The emergence of the Chinese market has brought about a completely different layout of the global industrial structure. Then there is the entrepreneurial environment. The most dangerous thing for a startup company is two things. The first is how to start the market. The product must not be perfect. Who is your white mouse customer? Playing a big company is a dead end. You must have small and medium-sized companies to accompany you. China has a large number of such customers, but in Europe and the United States, almost all of them are big company brands; the second is money, the same money is burned in Silicon Valley and in China. It can be many times more efficient. The company spends a long time to burn money, and the gas will grow, and the long gas will bring opportunities. Many returnee companies survive because of the long gas. Entrepreneurship in China: Weather + Location + People When I went abroad in 1989, there were hundreds of semiconductor factories in China. When I returned to China in 2000, I saw that these factories were almost gone, which surprised me. Faced with this kind of market, it is like going to Africa to sell shoes. A pessimist sees that no one here wears shoes, so let's not do it. But in the eyes of optimists, this is called a blank market, and there is opportunity here. And we are optimists. It was the PC era, and the boss was Intel. But we see that the next era must be the mobile phone, because the mobile phone is a handheld computer, and its market and influence must be greater than that of the PC. If we can make the core chip of mobile phones, then we must be the king of the mobile phone era. In 2001, we founded Spreadtrum Communications. During this entrepreneurial process, we have done a lot of things. Among them, there are two key strategies, which have played a decisive role in the development of the company. First, start from the 2G market. At that time, there was no domestic venture capital, and our money had to be taken from Silicon Valley. When the 3G standard just came out, we said we wanted to do 3G. Later, we got an investment of more than 6 million US dollars and went back to China. At that time, China's 2G market was the largest market in the world, and if we did it, we could do it. 3G is a new technology, and it is very difficult to do it. After consideration, we decided to do 2G first, which is one of our most critical decisions. Later, we used 2G sales to support 3G for ten years. At that time, among the more than a dozen companies in the world that did 3G with us, only we survived, precisely because we made the decision to make 2G first. When we were doing 2G, there was a particularly painful thing. After the chip was made, there were no customers in China who could make mobile phones. How to do? We have to do everything our customers can't do. We need to make the chip, make all the software inside, make the PCB, design the mobile phone case, go to the Ministry of Information Industry of that year to pass all the tests, and then get the license. Finally, we put a complete set in the hands of the customer and let them go into production. They only need to do two things, one is to change the appearance, and the other is to replace the splash screen with their company's logo. Overnight, hundreds of mobile phone manufacturers appeared in Shenzhen, which was called the Shanzhai mobile phone market. Before us, mobile phone chip manufacturers could only be made by Fortune 500 companies such as Texas Instruments, Qualcomm, Philips, and Siemens. Mobile phone design companies are also big brands such as Motorola and Nokia, and it takes about two years for them to design a mobile phone, which takes a lot of manpower and material resources. back. But we can make a mobile phone in about 4-6 months, and we can make money as long as we sell 10,000 units. Another very important point is that in those days, it cost at least two or three thousand yuan to buy a mobile phone, which is generally affordable by those above the white-collar workers. But we suddenly lowered the price to four or five hundred, so everyone can afford it. It can be said that we have rewritten the "rules of the game" in the mobile phone market. Second, return to China to start a business. At that time, among the dozen or so chip companies, 5 were founded by Chinese, and 4 of them were in the United States. Only Spreadtrum returned to China to do it. Only after returning to China can we discover a copycat market. If we start a company in Silicon Valley and then want to support the Chinese copycat market, it is almost impossible. In 2007, Spreadtrum was successfully listed on Nasdaq.

Start a business again: venture capital fund/industry M&A fund

In the process of starting a business, we found that what China lacks the most is the venture capital environment. Why is Silicon Valley so prosperous? Because it created a system of venture capital. Any technology company needs at least one or two years to do technology research and development, and another year or two to do product development, plus market development, and it usually takes three to five years to burn money. After we returned to China, we found that there was no domestic venture capital. Many bosses basically "invest in the current year", that is, to build factories in the same year and see benefits in the same year. But this is almost unrealistic. Like China's top technology enterprise and ZTE, they are all by chance, and batches are impossible. The companies that actually make technological innovations in batches must wait until China's domestic venture capital system emerges. In 2005, a number of venture capital institutions such as Northern Lights, Jinsha River, Sequoia, and SAIF Fund appeared in China, but they were all US dollar funds. After the GEM came out in 2009, many RMB funds appeared. Now RMB funds have accounted for more than 90%, becoming the absolute mainstream. At the time, we thought to ourselves that we had already started businesses twice, and we especially wanted to support the younger generation to start their own businesses. And many of our juniors and juniors have come back from the United States and are excited to do things, but have no money, so we feel that we should become VCs next to nurture them. In 2010, we established Huashan Capital. In 2014, the state increased its support for the semiconductor industry and established the Integrated Circuit Industry Fund. This is another historic opportunity for us. We established Qingxin Huachuang to manage part of the Beijing Semiconductor Industry Fund.

Investment Opportunities and Strategies in China's Semiconductor 2.0 Era

I think the development process of Chinese chips can be roughly divided into four stages: 1958-1979 is closed development, 1979-2000 is a difficult transition, 2000-2013 is a market-led barbaric growth period, 2014-2021 is a national / A period of rapid development jointly promoted by the government and the market.

1.0 era: market-dominant stage, brutal growth (2000-2013)

In the 1.0s, it was the market-dominant stage, and many semiconductor startups emerged, among which design companies were the most, because it was the easiest to do. At that time, many companies defined products wrongly. Later, a few companies figured out the rules and remade low-end products, and they all survived. Enterprises such as Zhaoyi Innovation and Zhuoshengwei all took detours in the past few years and then came back. Generally speaking, it was an era of brutal growth of semiconductor startups, and basically everyone concentrated on consumer electronics. The reason is very simple. Only this segment of the market is open. For other industrial applications such as white goods and communication base stations, customers do not open the market to you.

2.0 Era: State Support + Marketization (2014-)

In the 2.0s, we found that the development of the integrated circuit fund has exceeded our expectations. At the beginning, we thought that a fund within the state-owned system could invest in good projects? In the end, it was found that it solved several major problems. One was the construction of foundries, which our socialized capital could not do. The second is that it has invested in about ten sub-funds, including our Yuanhe Puhua. It is an aircraft carrier, and the sub-funds invested in it invest in some early funds around its aircraft carrier to cultivate the products below. Since 2014, almost all direct government investment projects have disappeared, and everyone has invested in the form of industrial funds. With this layer of constraints, whether the mayor has the final say or the market has the final say, there has been a big change. This is a fundamental change in China's investment system from a planned economy to a market economy, and it is also a way for government money to leverage social capital and establish a mixed fund together.

Characteristics of the 2.0 Era

(1) Entrepreneurial innovation and upgrading In the early days of the 1.0 era, most of the entrepreneurs were overseas returnees. They worked as engineers in large international companies, developed products, and mastered advanced technologies, but they had no market experience and management experience, nor did they understand the domestic market. In the 2.0 era, after more than ten years of development, large international companies (and domestic leading enterprises) have trained a large number of talents. The entrepreneurs we have seen in the past few years have all worked in large companies. Many of them have achieved the positions of general managers, directors or vice presidents. They all came out with products, customers, resources and even teams, so it will be greatly shortened. Time for detours. (2) Domestic substitution and upgrading In the early days of the 1.0 era, the domestic market was almost completely occupied by foreign products. This was the first opportunity for a chip startup company to staking a horse. The vast majority of startup companies choose the consumer electronics market with low technical threshold and fast acceptance by customers, such as mobile phones, MP3, PAD, etc. After a few years, these markets were quickly replaced by domestic products. In recent years, leading companies in various industries in China have discovered that domestic substitution is not only a matter of cost saving, but also a key factor in the safety of the supply chain and determines the life and death of the company. Therefore, the demand for domestic substitution has skyrocketed, and many blank markets have appeared almost overnight, including home appliances, industry, automobiles, power supplies, communication base stations, etc. This is the second opportunity for chip companies to staking the field, and the window period is only 5-10 years. Since then, in each market segment, one or two companies will gain a firm foothold, and the pattern of the domestic semiconductor industry will be basically determined. (3) Industrial mergers and acquisitions integration In the 1.0 era, there are thousands of semiconductor startup companies in China, which are generally small and scattered, grow wildly, and compete fiercely, but there are few mergers and acquisitions among their peers. At the same time, the domestic securities market is very abnormal, and it is extremely difficult for technology companies to go public, which seriously affects the emergence of leading companies and restricts the emergence of industrial integration. In 2019, the establishment of the Science and Technology Innovation Board greatly improved the situation. In the past year, more than 20 semiconductor companies have been successfully listed (2016-18, only 1-2 companies are listed each year), and a number of leading companies with a market value of over 100 billion have emerged, and they have also begun to actively deploy industrial mergers and acquisitions. It is foreseeable that after 5-10 years, the semiconductor industry will enter a mature stage of development: around dozens of leading companies, there are hundreds of thousands of start-up companies. Start-ups focus on the innovation of new technologies/new functions. Once the technologies/products are mature, large companies will acquire them at high prices and use their own market channels, supply chains, quality assurance and brand advantages to quickly open up the market and form a benign industry. cycle. In the future, the main exit channel for startups will be mergers and acquisitions (expected to be greater than 80%), rather than independent IPOs, which is a historically proven law of industry development. (4) Combination of government and private sector In the 1.0 era, most of the domestic semiconductor industry is driven by private capital. Since 2014, the government has begun to establish a semiconductor industry fund, which has been combined with private capital to invest in outstanding enterprises in a market-oriented way, and promote the industry to enter a period of rapid development. For strategic projects with huge investment and long payback period, it is difficult for private capital to invest, and the government's active action just fills this vacancy.

2.0 Era: Investment Opportunities and Investment Strategies in the Semiconductor Industry

Many people are asking, how many years will it take for China's semiconductors to catch up with the world's level? The answer I gave two years ago is that the packaging has basically caught up with the world level, the design will take 5-10 years, the memory will take 10-15 years, and the equipment/material will take 10-20 years. slow. There are roughly two types of investment opportunities in the 2.0 era:

One is domestic substitution. For example, mid-to-high-end chip design, production equipment, testing equipment, key components in corners and corners, etc., we are all doing these, this is an opportunity. The second is new markets and innovative products. Because of China's strong industrial chain and our fast action, we feel that all new hardware-related markets in the future will be formed and appear in China first. Including Bluetooth headsets, wearable products, home smart devices, 5G, AI, IoT, autonomous driving, and more. How to seize these opportunities? We think there are several key points: First, distinguish whether it is a market-oriented project or a strategic project. Many of the problems solved by stuck necks are really unprofitable or really small markets, which are strategic decisions of the country. The problems that the country needs to solve and our investment are two different things, and we must distinguish them clearly. Second, choose the investment stage that suits you, whether it is angel, early stage, growth stage, mid-late stage, and investment strategies are completely different. Third, keep an eye on three key points. There are three key points that are particularly important to the success of a company - angels, product success and customer acceptance. In the angel stage, you just meet each other. If you think the team is okay, you may vote. The success of the product proves that his technology and product are right. Customer recognition is another stage. When making investments, you must seize the inflection point of the company's value enhancement, and then invest in it. Fourth, do not chase the pigs on the wind. We must be vigilant about the Internet investment model and not follow the trend. Profit is the bottom line. Fifth, prepare for a protracted battle, gain an in-depth understanding of subdivisions, hone a precise vision, and tap companies with high growth potential to balance high valuations and increase their competitiveness. Sixth, accumulate experience and various resources to help investee companies grow. Can you invest in this company that you are interested in? Now you can’t invest if you have money. You have to think about how you can help. You have to accumulate your resources and connections, and make it special, and people will let you invest. Seventh, cooperate with leading professional funds to explore various new models to achieve a win-win effect of learning from each other and sharing resources. As a newcomer to investment, I highly recommend that you combine with the head fund. For example, you can give it some resources, it will meet your learning needs, so that you can get started quickly and the risk will be reduced a lot.

Finally, a word for everyone. This is also a word from the god of innovation, Jobs, to every entrepreneur. It is called Stay hungry, Stay foolish. There are many Chinese translations of this sentence. One of our alumni said, isn't this the school motto of Tsinghua University, "Unremitting self-improvement and great virtues".

Disclaimer: This article is reproduced from "Zingke Dune Academy" to support the protection of intellectual property rights. Please indicate the original source and author of the reprint. If there is any infringement, please contact us to delete it

Site Map | 萨科微 | 金航标 | Slkor | Kinghelm

RU | FR | DE | IT | ES | PT | JA | KO | AR | TR | TH | MS | VI | MG | FA | ZH-TW | HR | BG | SD| GD | SN | SM | PS | LB | KY | KU | HAW | CO | AM | UZ | TG | SU | ST | ML | KK | NY | ZU | YO | TE | TA | SO| PA| NE | MN | MI | LA | LO | KM | KN

| JW | IG | HMN | HA | EO | CEB | BS | BN | UR | HT | KA | EU | AZ | HY | YI |MK | IS | BE | CY | GA | SW | SV | AF | FA | TR | TH | MT | HU | GL | ET | NL | DA | CS | FI | EL | HI | NO | PL | RO | CA | TL | IW | LV | ID | LT | SR | SQ | SL | UK

Copyright ©2015-2025 Shenzhen Slkor Micro Semicon Co., Ltd